Polymarket Settles a Market Incorrectly–Again

For the second time in six months, Polymarket has misfired on a major geopolitical market — this time declaring a phantom minerals deal between the U.S. and Ukraine.

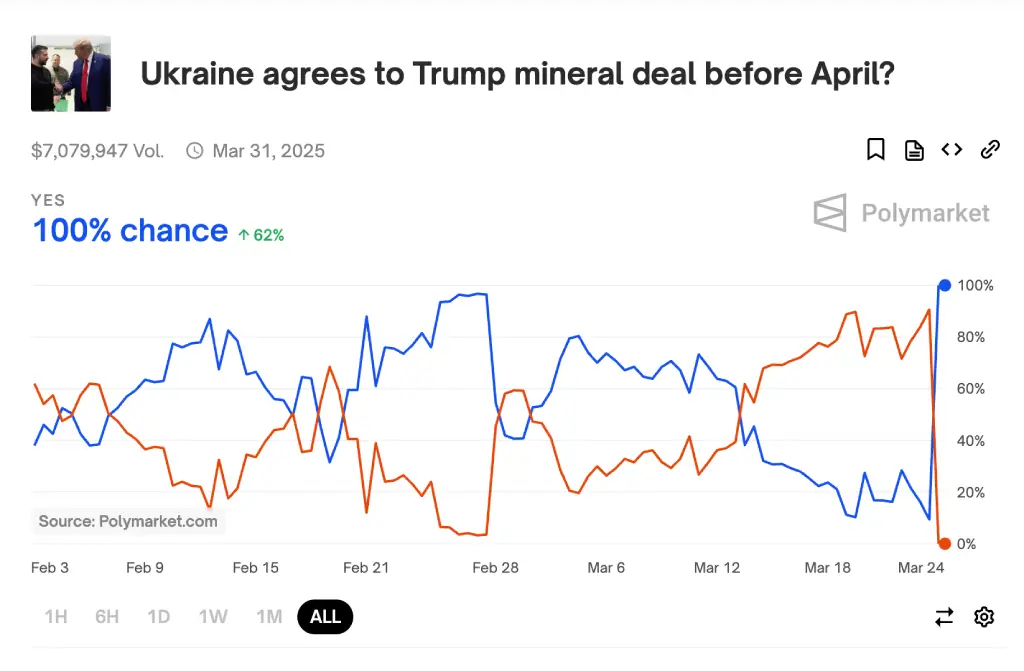

The market in question asked whether the United States and Ukraine would agree to a rare minerals deal between Feb. 2 and March 31. Reuters reported on Monday that Trump expected the two countries to reach a deal “soon,” but neither country committed to an agreement.

Consequently, Polymarket’s ‘No’ contracts were trading at about 84% on the evening of March 23. The next day, the odds were not only reversed, but the market resolved to ‘Yes’ – that Ukraine and the United States had reached a minerals deal.

According to the market’s terms, “An announcement of a deal will qualify regardless of if/when the deal is enacted.” No minerals agreement has been announced between the two countries. The market was resolved incorrectly.

In a statement on Discord, a Polymarket representative said:

“This is an unprecedented situation, and we have been in war rooms all day internally and with the UMA team to make sure this won’t happen again. This is not a part of the future we want to build: we will build up systems, monitoring, and more to make sure this doesn’t repeat itself.”

However, resolution disputes on Polymarket are hardly unprecedented.

History repeats itself

On Sept. 30, Israel launched a ground invasion in Lebanon to stop rocket fire from Hezbollah. Israeli officials and news outlets reported the invasion on Sept. 30, the final day before the market’s settlement deadline.

However, the outcome was disputed, and UMA, the organization that votes on resolutions through token-based voting on blockchain technology, made the final decision. While the majority of UMA voters believed the market should resolve to ‘Yes,’ token-weighted voting gave greater influence to a few high-stake participants—let’s call them “whales”—who voted ‘No.’ Their votes reversed the market’s outcome, angering traders and distorting the result.

Although Polymarket has committed to refining its rule-making and settlement process, CFTC-regulated competitor Kalshi, which resolves markets in-house rather than with a decentralized protocol, has not faced a dispute akin to Polymarket’s Ukraine or Lebanon markets. Kalshi drew some criticism for using initial broadcast figures to settle its Oscars viewership market rather than later-corrected figures, but it adhered to its own settlement criteria.

Polymarket’s struggle to establish consistent and transparent market resolution criteria comes at a time of increased scrutiny for the prediction market industry. The Commodity Futures Trading Commission (CFTC) is set to hold a roundtable on April 30 to help craft a regulatory framework that accommodates the new types of event contracts, including sports, now offered by prediction markets.

Though Polymarket operates outside of the CFTC’s jurisdiction, the shadow of its settlement disputes will likely loom over regulated markets as they make the case for their value at the agency’s April roundtable next month.